The Financial Scrutiny Unit provides independent analysis to support effective financial scrutiny in committees of the Senedd and to individual Members on budgetary trends and issues. This includes support for the costing of specific spending proposals, and research on all areas of the economy and public finances as they affect the Welsh Government and Senedd.

Financial Scrutiny

Financial Tools

Summaries of devolved funding, budgets and financial scrutiny

How Wales is funded – including composition

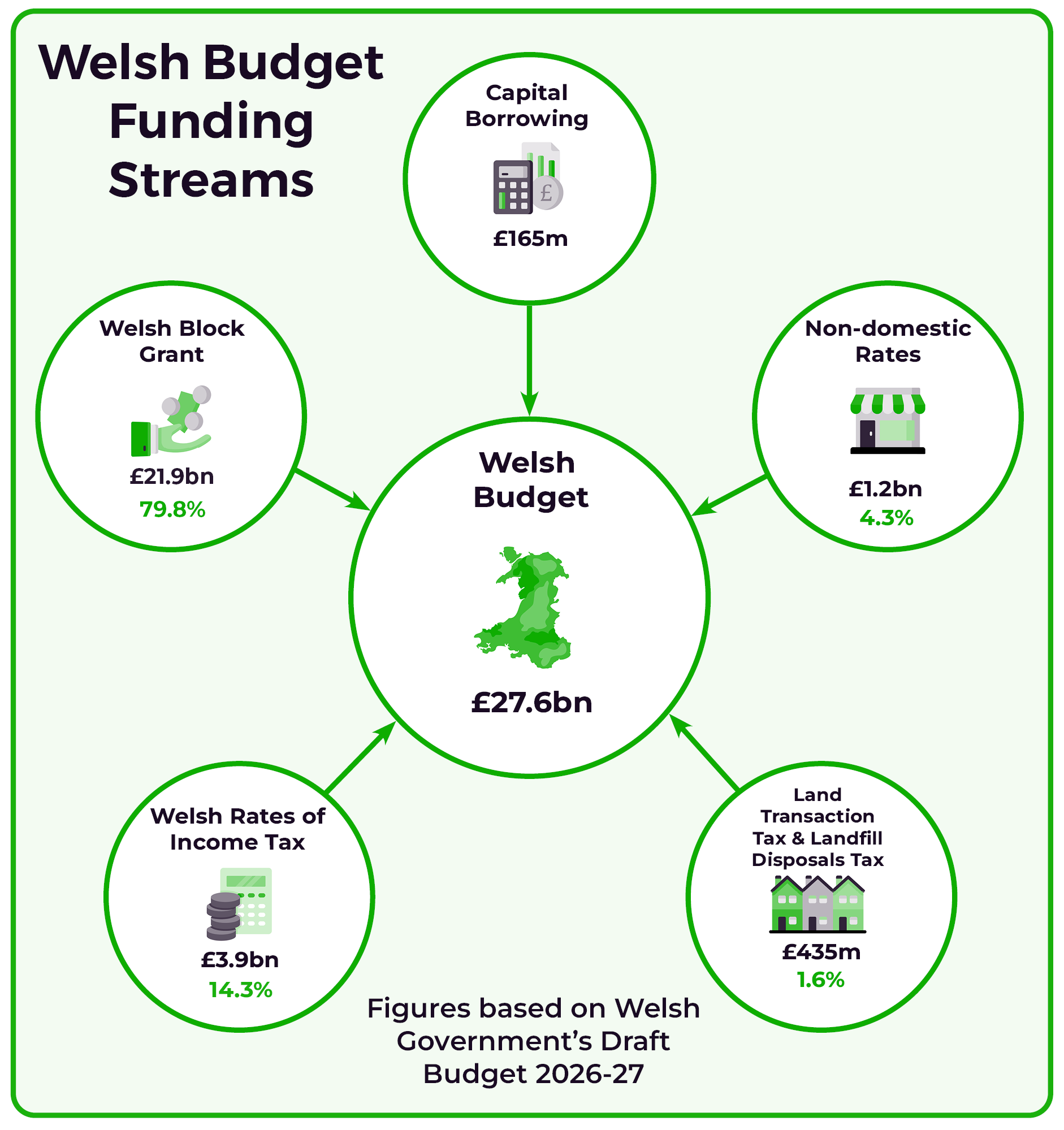

The Welsh budget is made up of multiple funding streams. The largest stream is the block grant received by the UK Government, which is calculated using the Barnett formula.

Welsh taxes enable the Welsh Government to raise 20% of its own revenue for public spending and increase its accountability to the people of Wales. Welsh Government is also able to borrow a limited amount per year to spend on capital projects.

Sources of Welsh Government funding for 2026-27

Source: Welsh Government explainer and Senedd Research

Barnett formula – including how consequentials work

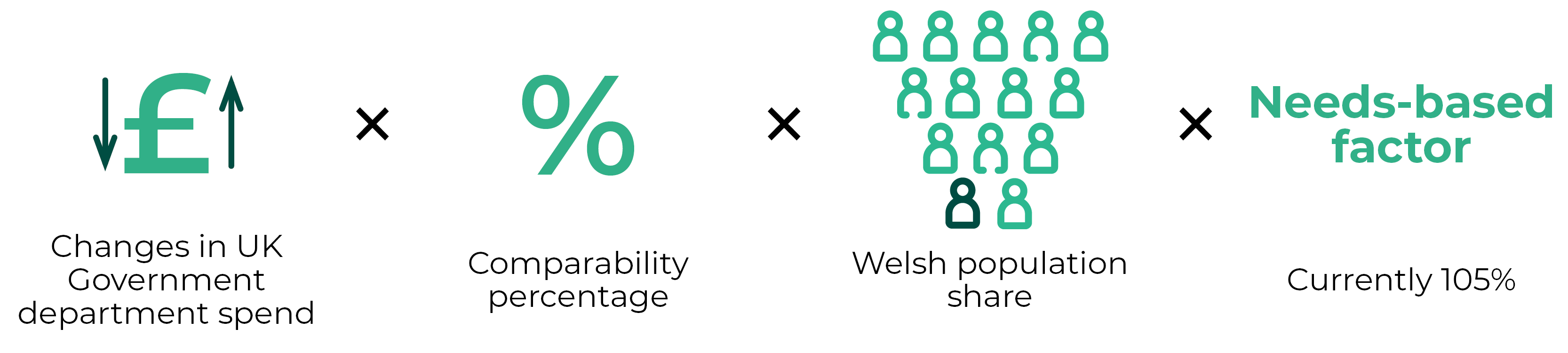

The Barnett formula is a mechanism used by HM Treasury to adjust the funding allocated to Wales through the block grant to reflect changes in public service spending by the UK Government in England. Funding increases announced by the UK Government in areas devolved to Wales would result in Barnett consequentials.

The Welsh Government agreed a fiscal framework with the UK Government in 2016, which established the Welsh Government’s funding arrangements to support its devolved fiscal powers. This set out a modified Barnett formula for Wales.

Barnett formula for Wales

The comparability percentage is the extent to which services delivered by UK Government departments are devolved to Welsh Government. The Welsh population share is the percentage of the Welsh population compared to the population of England.

The Barnett formula also includes a needs-based factor temporarily set at 105%. When funding relative to England has converged to 115% per capita this factor will be increased to 115%.

Fiscal devolution – including borrowing and reserves – new taxes

The Wales Act 2014 legislated to devolve tax powers to Wales for the first time in almost 800 years. It enabled the Welsh Government to legislate in respect of areas to which Stamp Duty Land Tax (SDLT) and Landfill Tax (LT) previously applied. These UK taxes were replaced by Land Transaction Tax (LTT) and Landfill Disposals Tax (LDT) respectively.

The Act also legislated for the partial devolution of income tax to Wales which was replaced by the Welsh Rates of Income tax (WRIT).

A Visitor Levy will also be introduced to Wales from April 2027. This will be charged on overnight stays in visitor accommodation and will only apply to areas where local authorities decide to implement it.

There will be a lower and higher levy rate depending on the type of accommodation visitors stay in with local authorities spending any revenue raised on sustainable tourism development.

What taxes could be devolved in the future?

The UK Government announced in its 2025 budget plans to introduce new rates of income tax on property income from 2027-28. It is the intention to devolve the setting of these rates in Wales to the Senedd in the future.

In 2014, the UK Government proposed to devolve the aggregates levy to Wales subject to the resolution of legal challenges. There has been no announcement on when this will happen.

Additionally, the previous Welsh Government wanted to introduce a new vacant land tax. However devolved competence is needed from the UK Government, which, despite being formally requested almost six years ago, is yet to be agreed, leading to criticism about the process.

Progress has finally been made, with a joint consultation between both governments expected to be published in 2026.

What borrowing powers does Welsh Government have?

The Welsh Government is able to borrow (within limits) for both resource and capital purposes. Capital limits increased by 10% from 2026-27 and will be annually uprated in line with inflation from 2027-28, whilst revenue limits are unchanged.

Resource borrowing

Welsh Government can borrow up to £200 million annually (within a total cap of £500 million) if tax revenues are lower than forecast. This has to be repaid in four years.

Capital borrowing

Welsh Government has a total borrowing limit of £1.1 billion with an annual borrowing limit of £165 million for 2026-27, which can be secured from the National Loans Fund (through the Secretary of State for Wales) or a commercial bank.

Government bonds

The Welsh Government also has powers to issue government bonds to borrow for capital projects, which count towards its total and annual capital borrowing limits.

How does the Wales Reserve work?

The Wales Reserve was established for Welsh Government to deposit unallocated resource or capital funds at the end of a financial year, which can be drawn down to fund future spending. The reserve is capped and held within the UK Government.

The total and annual drawdown limits have been increased by 10% from 2026-27 and will be uprated in line with inflation each year from 2027-28.

The total Wales Reserve limit is £385 million for 2026-27. There are no annual limits for payments into the reserve but the Welsh Government can only withdraw £137.5 million and £55 million for resource and capital spend respectively per year.

Resource funds deposited into the Wales Reserve can be used for both resource and capital spend but capital funds are limited to capital spend.

Block grant adjustment

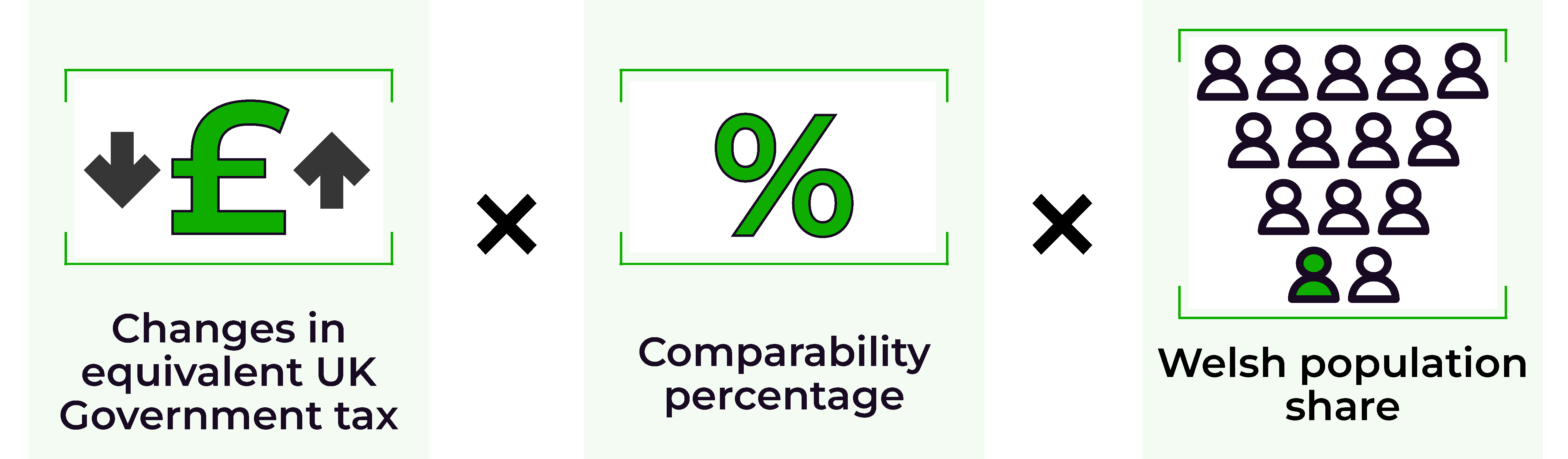

The partial devolution of income tax together with the devolution of UK Stamp Duty Land Tax and Landfill Tax to Wales meant the UK Government forfeited revenue raised by these taxes to Welsh Government, which now administers its own taxes. To compensate for this, a block grant adjustment is made to each of the devolved taxes using the comparable model.

Comparable model

If revenues collected from Welsh taxes grow at a faster rate than the equivalent UK taxes then Welsh Government would receive more tax revenue than the resulting block grant adjustment, which means more funding for the Welsh Budget and vice versa.

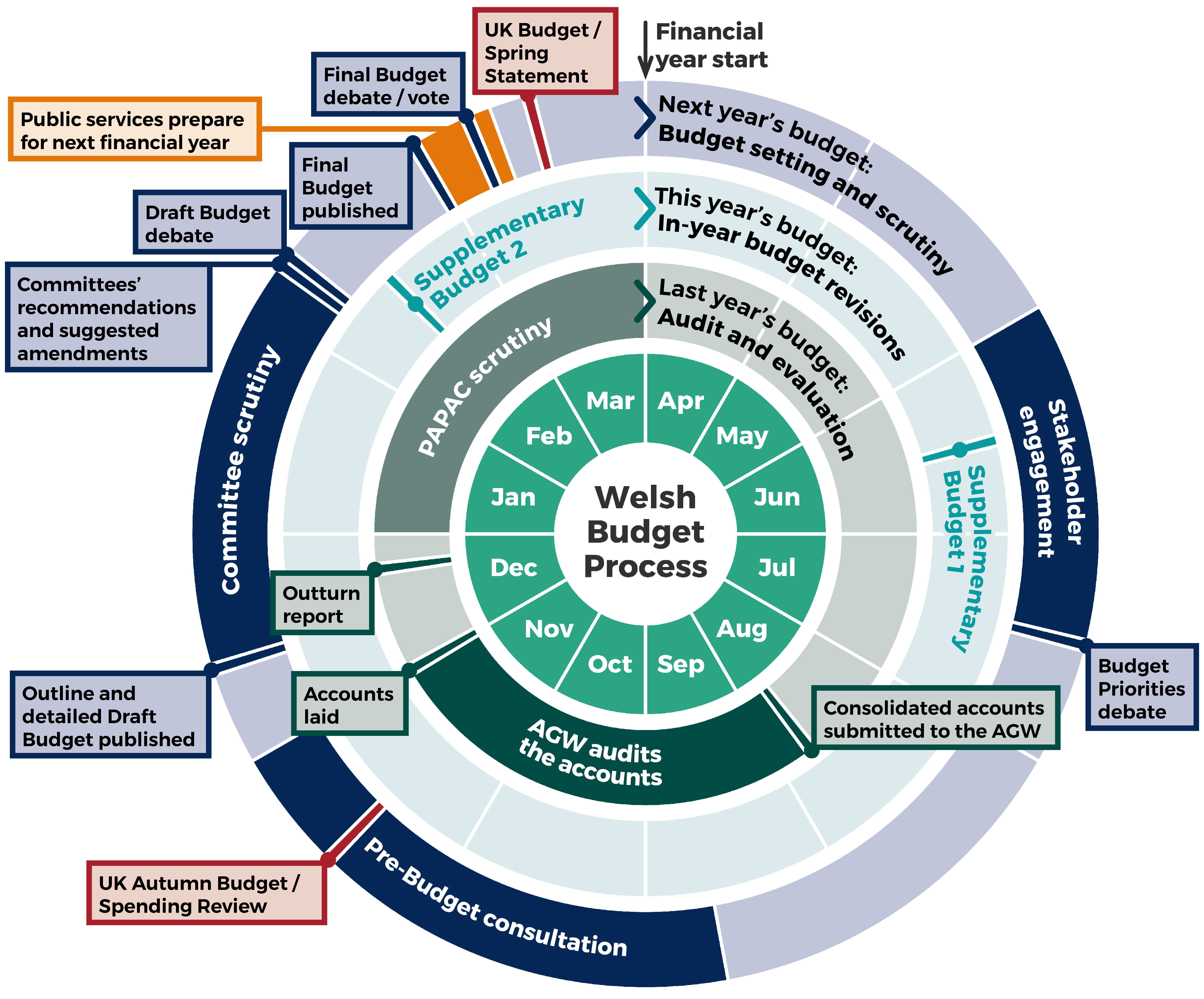

Budget process – including timescales and scrutiny

Every year the Welsh Government publishes their spending plans for the next financial year.

There is a year-round process of budget scrutiny, which allows Members of the Senedd to consider, influence and review the budget decision making at different times of the year.

Pre-budget

Before the draft budget is published, there is a Pre budget scrutiny phase where the Senedd’s Finance Committee engages with stakeholders and individuals.

This is followed by a budget priorities debate in the Senedd to raise the profile of issues to inform the Welsh Government’s own priority and budget setting process. This usually takes place in July.

Draft budget

A budget protocol agreed between the Welsh Government and the Senedd in 2017 sets out timing of laying their Draft Budget in “normal circumstances”. However, the UK Government has since changed to a single fiscal event at the autumn budget, where devolved funding is confirmed. This has led to the budget process usually following procedures for “exceptional” years.

The Welsh Government’s draft budget includes taxation and spending plans alongside the latest OBR devolved Welsh tax forecasts, which are scrutinised and reported upon by Senedd committees before a plenary debate.

Final budget

Following the Draft Budget debate, the Welsh Government lay a final budget, which is voted upon in the Senedd.

Supplementary budgets

The Welsh Government will usually publish two in-year supplementary budgets (normally in June and February), reflecting changes to funding. These supplementary budgets incorporate changes announced by the Welsh Government and any changes to funding from the UK Government. These supplementary budgets are scrutinised by the Finance Committee before a vote to approve is held in the Senedd.

Welsh Government accounts

The Welsh Government publish audited accounts towards the end of the calendar year, which are scrutinised by the Public Accounts Committee. Soon after an Outturn report is published which shows end of year spending compared to the latest approved budget.

Approximate budget and scrutiny timelines normal v exceptional year

Procedure for exceptional year.

In a “normal year” the Welsh Government will lay their budget in two stages, starting with an outline budget in October.

What happens if a budget motion is not agreed

If a Budget resolution for a financial year is not passed by the Senedd before the start of that financial year (1 April), then initially only 75% of the budget authorised to be used in the previous financial year is available.

The figure increases to 95% if a Budget resolution has not been agreed by the end of July.

An Annual Budget Motion can be tabled by a Welsh Minister and considered by the Senedd during the financial year to which it relates – so a budget for 2027-28 could be passed after 1 April 2027, if the Senedd had not agreed a budget by that point.

The budgets of directly funded bodies (Wales Audit Office, Public Services Ombudsman for Wales, Senedd Commission, and the Electoral Commission Wales) are also included within the annual budget motion.

In the event a budget is not agreed, these directly funded bodies, along with the Welsh Government, could only access 75% / 95% of their previous year’s budget until an annual budget motion was authorised.

Local authorities in Wales, which receive the majority of their funding from the Welsh Government, are legally required to set their budgets and council tax before 11 March in the financial year preceding the one to which the budget applies. This deadline ensures billing authorities can issue council tax bills in time for the start of the financial year on 1 April.

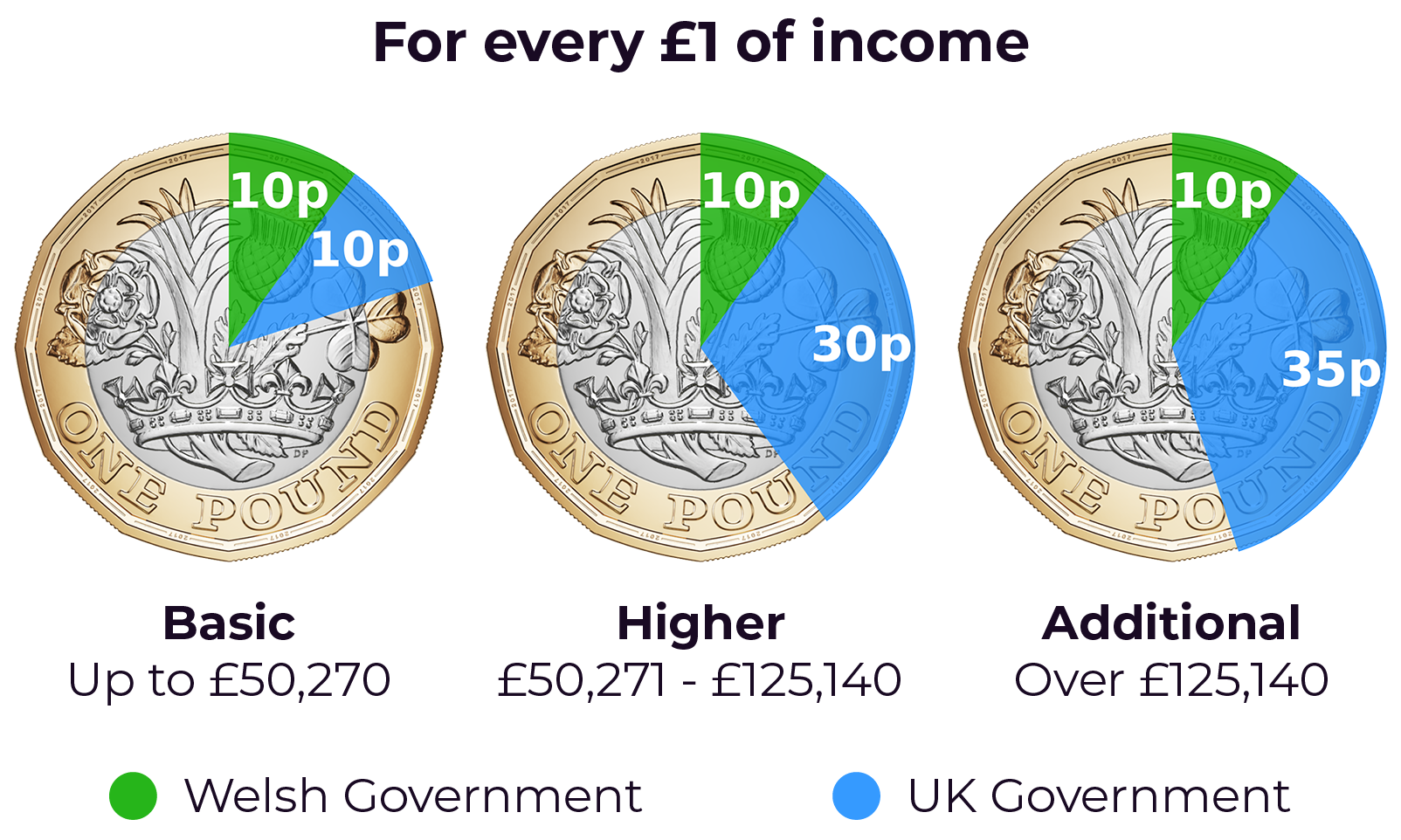

Welsh Rates of Income Tax (‘WRIT’) resolution

A resolution on the Welsh Rate of Income Tax (‘WRIT’) must be made before the start of the tax year, which begins on 6 April. It can only be made for one tax year and must apply to the whole of that tax year.

A Welsh rate resolution can only be considered once the Annual Budget Motion is published, but no earlier than 12 months before the start of the relevant tax year.

The Senedd cannot pass a budget until it has first agreed a Welsh rate resolution. This is based on the principle that the Senedd cannot take a decision on the spending plans contained in the Annual Budget Motion without first agreeing how the revenues to pay for those funds will be raised through taxation.

Once agreed, a Welsh rate resolution can be cancelled before the start of the tax year, but it cannot be cancelled or changed once the tax year it applies to has started, so from 6 April onwards.

We publish an interactive income tax tool after each Draft budget, found in the interactive tools, this show the impact of changing income tax rates and amounts much an individual taxpayer would pay in WRIT.

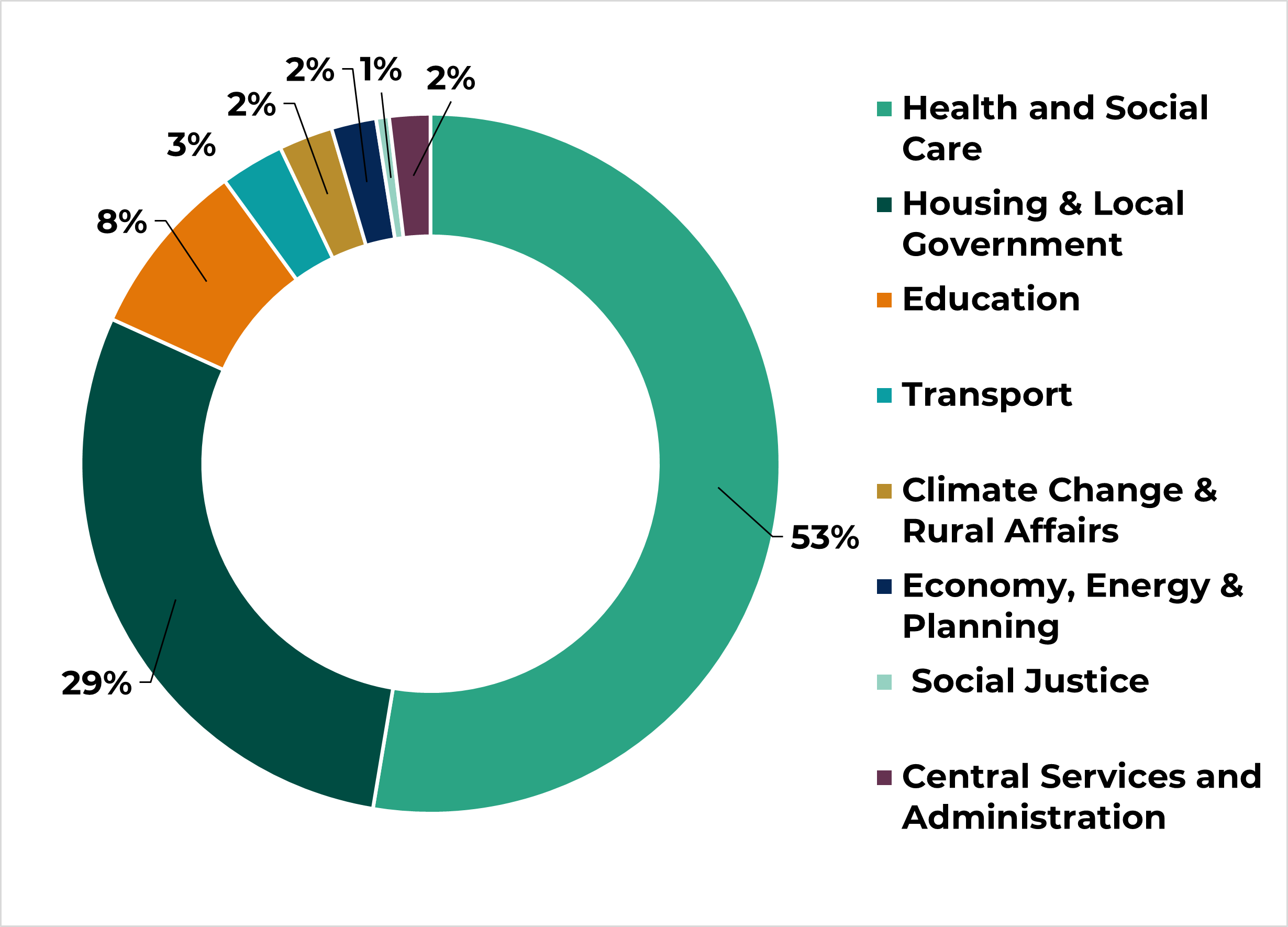

Where money is spent

More than half of funding from the Welsh Budget is allocated to the health service followed by almost a third to local government, which includes social care and schools.

We publish an interactive budget tool after each Draft budget, found in the interactive tools, this will have latest figures and breakdowns by budget line.

Financial scrutiny of legislation

A best estimate of the costs associated with delivering legislation introduced in the Senedd are set out in the Regulatory Impact Assessment (RIA) section of the Explanatory Memorandum, which accompanies the legislation.

The Presiding Officer must decide in every case whether a financial resolution is required for a Bill. This depends on whether the legislation requires new public money or significant additional funding for an existing service or purpose.

Only a Welsh Minister can move a financial resolution and if the resolution isn’t passed by the Senedd then the legislation ‘falls’ and will not be considered further.

The Finance Committee also considers the financial implications of Senedd Bills through its scrutiny sessions with Members in charge of the legislation. This is usually Welsh Ministers responsible for Government Bills and Members of the Senedd who introduce Private Member Bills.

The Committee publishes a report making recommendations to the Member in charge, which the Member responds to. The report is considered when the Senedd votes on the general principles of the bill and the financial resolution.

Welsh Government Budgets

The Welsh Government sets out its spending and financing plans for the forthcoming financial year in the autumn.

The Senedd scrutinises the budget and associated taxation and spending plans.

Tax Devolution timeline

The Wales Act 2014 legislated to devolve tax powers to Wales for the first time in almost 800 years. It enabled the Welsh Government to legislate in respect of areas to which Stamp Duty Land Tax (SDLT) and Landfill Tax (LT) previously applied. These UK taxes were replaced by Land Transaction Tax (LTT) and Landfill Disposals Tax (LDT) respectively.

The Act also legislated for the partial devolution of income tax to Wales which was replaced by the Welsh Rates of Income tax (WRIT).