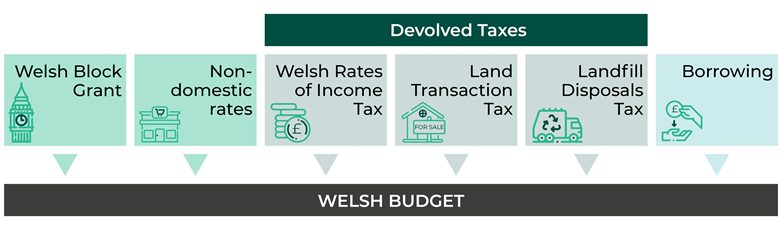

The Wales Act 2014 legislated to devolve tax powers to Wales for the first time in almost 800 years. It enabled the Welsh Government to legislate in respect of areas to which Stamp Duty Land Tax (SDLT) and Landfill Tax (LT) previously applied. These UK taxes were replaced by Land Transaction Tax (LTT) and Landfill Disposals Tax (LDT) respectively.

The Act also legislated for the partial devolution of income tax to Wales which was replaced by the Welsh Rates of Income tax (WRIT).