The Seventh Senedd will see the devolution of new taxes to Wales, and a push for new income tax powers to give the Welsh Government greater control over how funding is raised for the Welsh Budget. Could the devolution of the Crown Estate and its revenues also add to the funding pot in the Seventh Senedd?

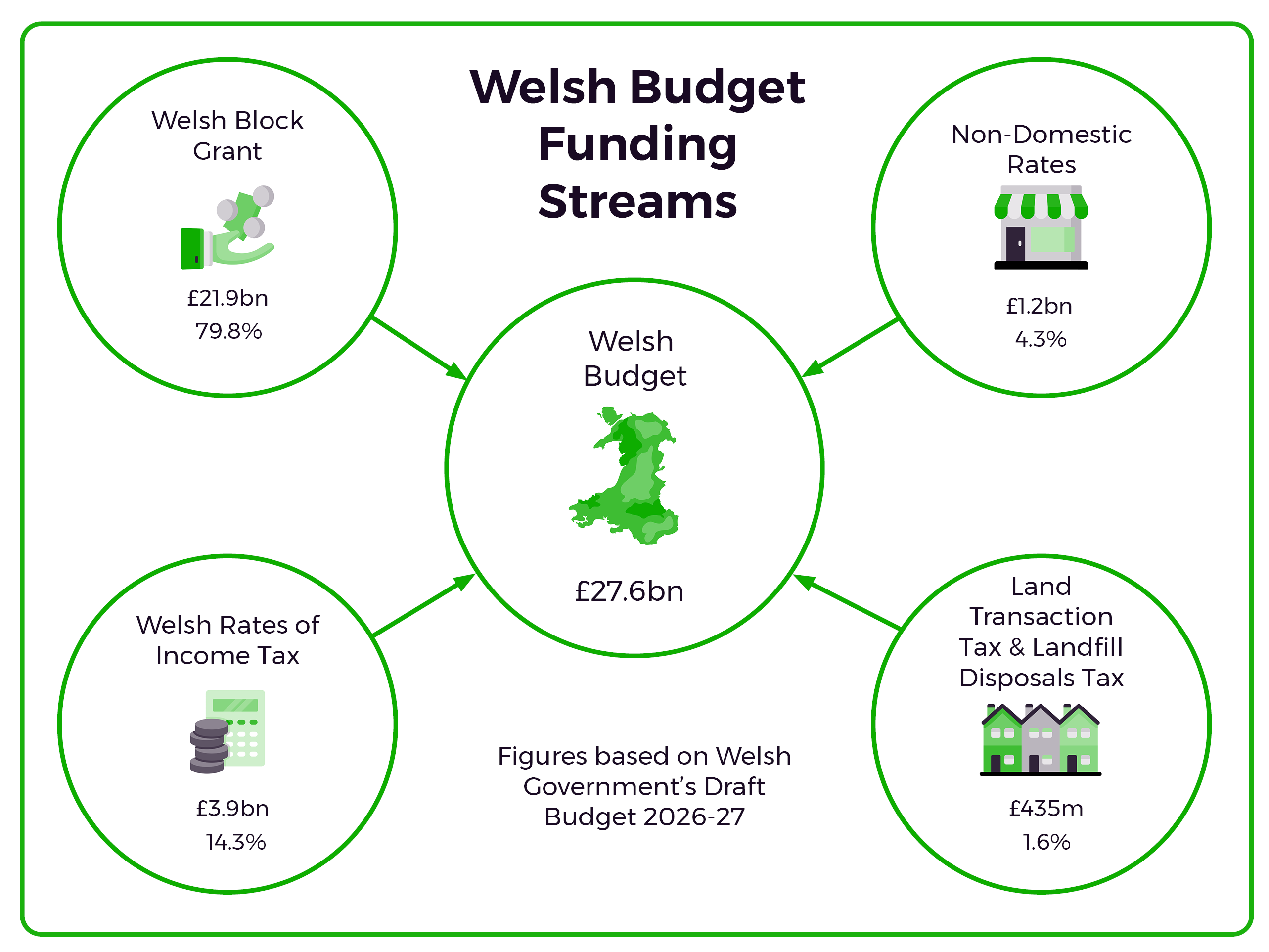

Fiscal devolution, which gives Welsh Government tax-raising and borrowing powers, has reshaped how Wales is funded. Devolved taxes account for around a fifth of the Welsh Government’s budget, yet progress in expanding these powers has been slow.

New tax proposals, questions around income tax flexibility, and a continued debate around the devolution of the Crown Estate all point to a period of potential change during the Seventh Senedd.

Incoming Members will face important decisions about how far Wales should go in shaping its own revenue-raising powers, and how these tools can support wider national priorities.

Figure 1: Sources of Welsh Government funding, 2026-27

Source: Welsh Government explainer and Senedd Research

The current landscape of Welsh taxes

The 2016 Welsh fiscal framework sets out the Welsh Government’s funding arrangements across its tax and spending responsibilities. This includes additional capital borrowing powers, and a Wales Reserve to help the Welsh Government manage its budget.

In 2018, Land Transaction Tax (LTT) and Landfill Disposals Tax (LDT) replaced UK Stamp Duty Land Tax and UK Landfill Tax respectively. LTT is payable when purchasing property in Wales, and LDT is a tax on the disposal of material to landfill and is payable by landfill site operators. Revenue collected from both taxes raises almost 2% of the Welsh budget.

In 2019, income tax was partially devolved to Wales and replaced by Welsh Rates of Income Tax (WRIT). Revenue raised through WRIT funds over 14% of the Welsh budget.

Wales has gained a modest suite of tax powers in recent years, but with almost 80% of the Welsh Government’s budget coming from the block grant (which comes from the UK Government), how far do current Welsh taxes empower Welsh fiscal policy?

What taxes are coming to Wales?

The UK Budget 2025 announced changes to UK taxation of income from assets, creating separate tax rates for property income from April 2027.

The tax will be devolved to Wales, with the Welsh Government able to set the rates but not the thresholds (like WRIT, discussed below). It’ll be payable by anyone living in Wales, regardless of where their rental properties are.

The tax will provide the Welsh Government with another lever on its fiscal devolution journey, but how landlords might respond is unclear, and how a divergence in rates between Wales and England could impact the rental sector in Wales is unclear.

Additionally, the previous Welsh Government wanted to introduce a new vacant land tax. However devolved competence is needed from the UK Government, which, despite being formally requested almost six years ago, is yet to be agreed, leading to criticism about the process.

Progress has finally been made, with a joint consultation between both governments coming soon. The previous Cabinet Secretary for Finance and Welsh Language, Mark Drakeford MS said:

The consultation will be launched, I think, very quickly after the Senedd elections. It’ll be a short and technical consultation, and then, hopefully, we’re on the home straight so that this power can be devolved to Wales, and the Senedd can then decide whether or not it wishes to use it.

What does this mean for the Seventh Senedd? The pace of negotiation suggests movement, but how fast? And will this tax incentivise developers and have a meaningful impact on Welsh housing?

Income tax powers: are they fit for purpose?

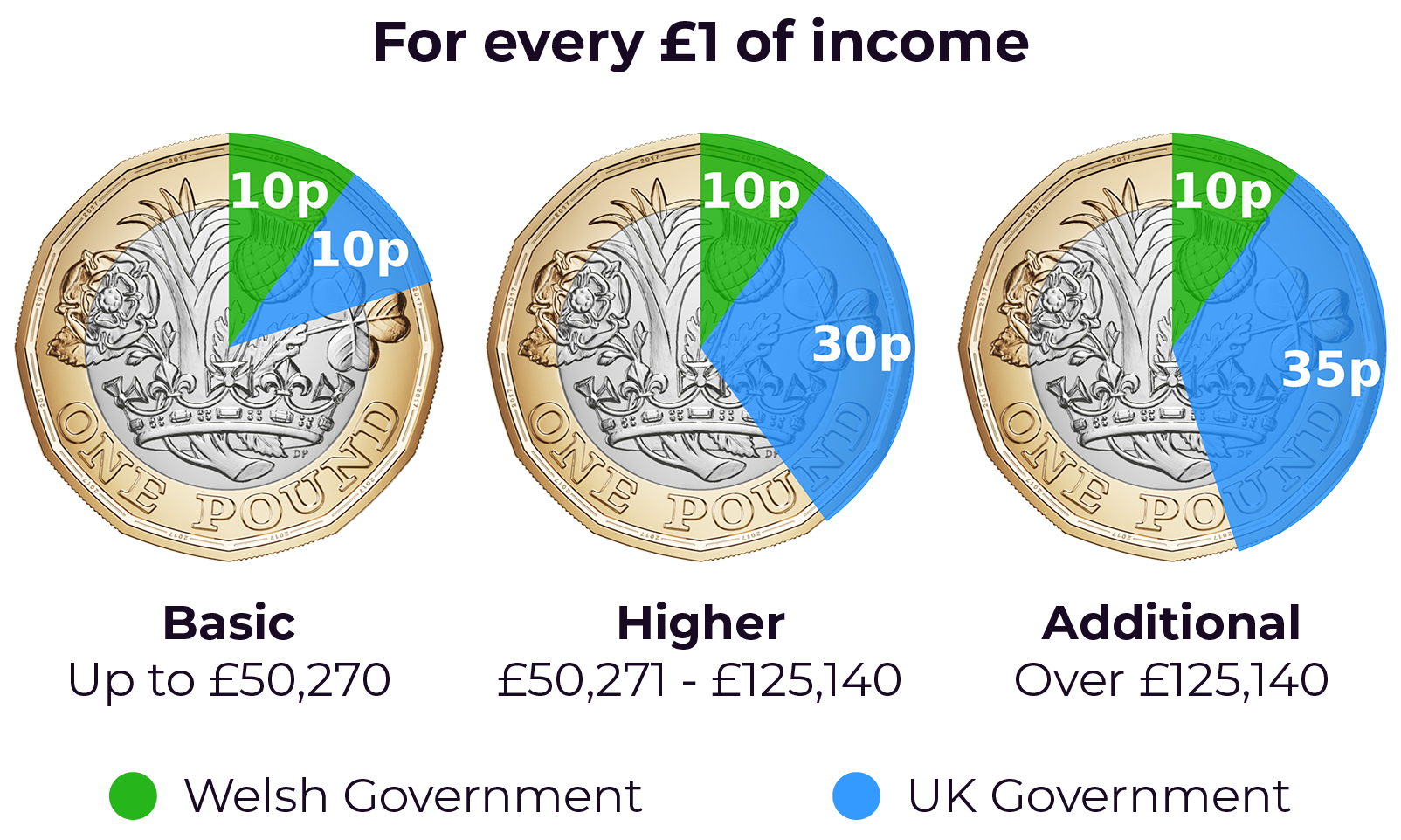

Welsh Rates of Income Tax (WRIT) gives the Welsh Government control over 10p of income tax for each rate. The Welsh Government has powers to change the tax rate to increase or decrease revenue, but not the thresholds or create new tax rates.

Figure 2: How WRIT works

Source: Welsh Government Outline Draft Budget 2026-27 Report and Senedd Research

The then Cabinet Secretary noted that powers to change the income tax rate have never been used, and he finds it “difficult to see the circumstances where they would be used”.

The income tax thresholds are based on UK Government policies and do not take into account different income profiles across nations. There is a higher proportion of taxpayers in Wales who only pay the basic rate of income tax compared to the whole of the UK with the UK having a greater proportion of taxpayers paying higher and additional rates of income tax compared to Wales. Consequently, the current powers don’t allow the flexibility to develop a balanced approach for taxpayers in Wales.

Scotland has more income tax powers than Wales, with the Scottish Government able to adapt income tax thresholds and create new tax bands to tailor its income tax policies. This means that Scotland has more scope to target revenue from tax rises or cuts.

Are these the powers Wales needs? Research on whether there are more usable income tax powers found that, although greater income tax powers would give more control, it would increase the level of risk to the Welsh Government if, for example, wages grow more slowly in Wales than in England and Northern Ireland.

Greater income tax powers could allow Wales to design a system more suited to its income distribution. But could the added risk make future budgets less predictable? The Seventh Senedd may need to weigh flexibility against stability.

The Crown Estate debate: offshore opportunities for a new revenue source?

The Sixth Senedd has seen the debate intensify over the devolution of the Crown Estate with much of it centred around the premise that devolution would unlock significant renewable energy revenue for Wales.

The Crown Estate is a collection of marine and land assets and holdings belonging to the reigning monarch. Its total asset value in Wales was reported to be £853m in 2022-23, with offshore wind and marine energy making up 93% of these assets.

In terms of revenue, the Crown Estate receives annual payments from developers for seabed rights during the project development phase. Once the project is operating, the Crown Estate charges a rent based on 2% of the project’s revenue generated per year. Wales currently has three offshore wind farms located off the north Wales coast.

With major offshore projects, such as the Llŷr and Erebus floating wind farms, planned off the Pembrokeshire coast, and the potential for further projects, the devolution of the Crown Estate would provide an additional funding stream for the Welsh Budget. Consequently, the Welsh block grant would be adjusted to account for the Welsh Government taking control of this revenue.

The Crown Estate was devolved to Scotland in 2017. Crown Estate Scotland manages assets valued at £665m as of 31 March 2024, which generated approximately £135m in income in 2023-24, with the majority used for public spending. Revenue generation is only one of the benefits, with Crown Estate Scotland saying its estate could enable:

£96.1bn in investment over the next 10-15 years in the offshore wind energy sector. This could generate at least £15.7 billion GVA and annually support 21,200 jobs.

In 2024, the Independent Commission on the Constitutional Future of Wales recommended the Crown Estate “should become the responsibility of the devolved government of Wales, as it is in Scotland”. If not devolved, will Wales miss opportunities to shape and capture value from its own natural resources?

Wales’ fiscal journey: what does the future hold?

The Seventh Senedd will face key choices about Wales’ fiscal future. New taxes may offer more control, but also bring uncertainty about how people and markets will respond. Limits to current income tax powers, and ongoing debate over the Crown Estate, highlight potential opportunities for Wales to further shape and benefit from its own revenue sources. Incoming Members will need to balance the opportunities of greater fiscal autonomy, with risks it may introduce.

Article by Christian Tipples, Senedd Research, Welsh Parliament