The Non-Domestic Rating (Chargeable Amounts) (Wales) Regulations 2016 (the regulations) will be discussed and voted on in Plenary on 12 December 2016. These set out the Welsh Government’s transitional relief scheme for small businesses negatively affected by the upcoming business rates revaluation due to come into force on 1 April 2017, which has been a hot topic over recent weeks.

What is the business rates revaluation, and what impact does it have on business rates bills?

Business rates revaluations usually happen every five years, and the Valuation Office Agency (VOA) is independently conducting a revaluation of all non-domestic properties in Wales to come into force from April 2017, based on their rateable value as at 1 April 2015. The Welsh Government highlights that a revaluation is revenue neutral and redistributes business rates liabilities in a way that reflects changes in the property market, rather than seeking to increase revenue raised from business rates.

The rateable value of properties in Wales has decreased between the 2010 valuation and the 2017 draft valuation. There has been a 2.9% decrease in rateable values on the local rating list (the vast majority of properties), however this decrease is offset by a 25.8% increase in rateable value of the properties on the central list such as major utilities and telecoms firms.

Businesses across Wales have been able to access their draft valuations on the VOA’s website from 30 September 2016. Revisions to draft rateable values can be made between October 2016 and March 2017, if there are factual errors in the valuation. Appeals against valuations can be made from April 2017.

The amount of business rates that must be paid on a non-domestic property is calculated in the following way in Wales.

The Cabinet Secretary for Finance and Local Government has stated that the multiplier for Wales will provisionally increase from 0.486 in 2016-17 to a provisional multiplier of 0.499 in 2017-18. Therefore, before any reliefs that a business may receive are considered, changes in their business rates bill in 2017-18 are determined by the change in its rateable value and the change in the multiplier.

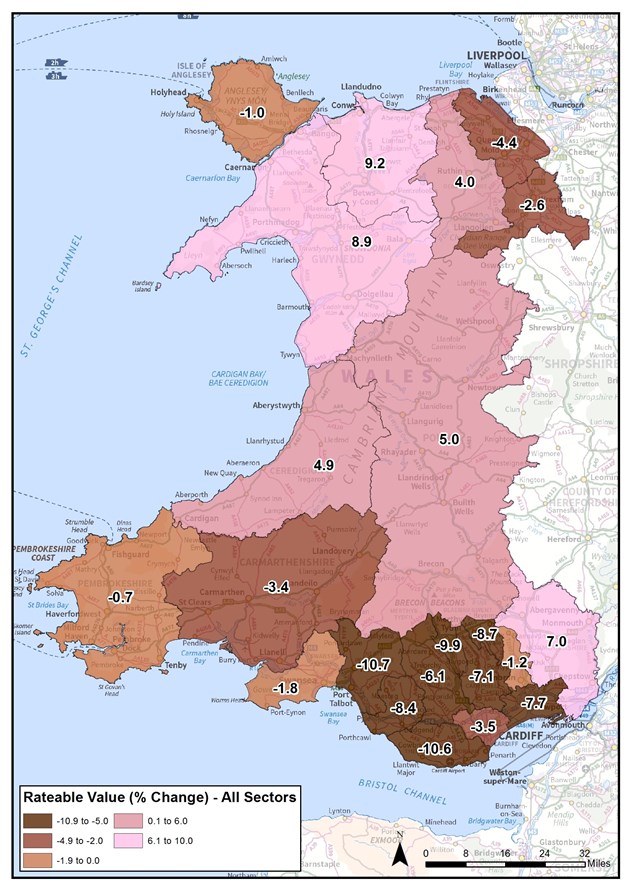

How have different parts of Wales been affected by the business rates revaluation?

The VOA have published maps of the average percentage change in rateable value in each local authority between the 2010 valuation and the 2017 draft revaluation figures, and these are set out below. When looking at these figures, it is important to note that the impact on particular sectors in local authority areas may be different. Also, the figures are averages and while some businesses in all local authority areas will have seen increases in their rateable value, others will have seen decreases in their rateable value.

How will the Welsh Government’s proposed transitional relief scheme operate?

The Cabinet Secretary for Finance and Local Government has released a written statement outlining transitional relief for small businesses who will no longer receive as much small business rate relief as they currently do from April 2017. Businesses who currently have premises with a rateable value of up to £12,000 and are eligible for small business rate relief in 2016-17, but will receive either less or no relief in 2017-18 due to the rateable value of their property increasing will benefit from this scheme. More than 7,000 ratepayers will benefit from this support, and it will be fully funded by the Welsh Government at a cost of £10 million.

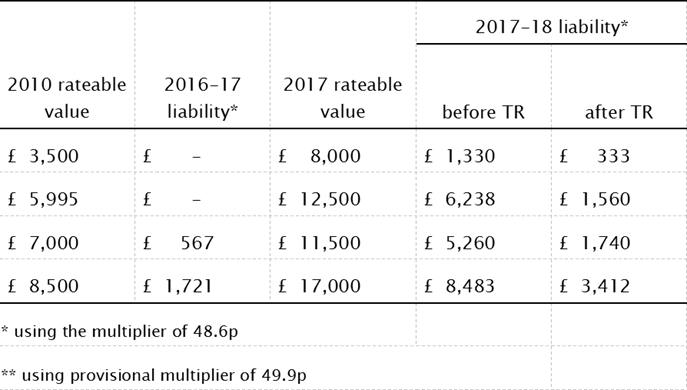

The proposed transitional relief will spread increases in business rates liability over a three-year period, so businesses will pay 25% of their increased liability in 2017-18, 50% in 2018-19 and 75% in 2019-20. By the start of the 2020-21 ratepayers will pay their full bill based on the 2017 revaluation. Examples of how the relief will work in practice are set out in the table below from the explanatory memorandum to the regulations.

This is different to the scheme proposed by the UK Government for England. Under this scheme, it is proposed that all businesses who see an increase in their business rates bill as a result of the revaluation will receive some transitional relief. This is a self-financing scheme, which is paid for by capping the reductions that businesses who see a decrease in their bills will receive.

The Welsh Government considers that its scheme is simpler than the one proposed in England, allows those businesses who have seen a reduction in their business rates liabilities to receive the full reduction, and means that all ratepayers will be paying their full liability before preparations commence for the next revaluation.

Comparative analysis of who would benefit most in Wales from both of these schemes set out in the explanatory memorandum. The Welsh Government’s proposed scheme benefits the following groups:

- Iron and steel works; surgeries and health centres; power generators and shops which do not sell food. On average these groups will see a decrease in their rateable values on average following the 2017 revaluation;

- Businesses in Merthyr Tydfil, Neath Port Talbot and Newport, who will see average decreases in their rateable value of more than 7% following the 2017 revaluation.

If the Welsh Government adopted a scheme the same as that proposed in England, then this would benefit properties with a rateable value of over £12,000 that have seen an increase in their liability, especially in the following groups and areas:

- Universities; car parks; hotels; libraries and museums; who will, on average, see an increase in their rateable values following the 2017 revaluation;

- Businesses in Gwynedd, Conwy and Monmouthshire, who will see average increases in their rateable value of more than 7% following the 2017 revaluation.

Article by Gareth Thomas, National Assembly for Wales Research Service