Article by Megan Jones, National Assembly for Wales Research Service

Debt levels are increasing in Wales, and are particularly high in certain areas. Financial exclusion is also a problem. What can be done to tackle both these issues during the Fifth Assembly?

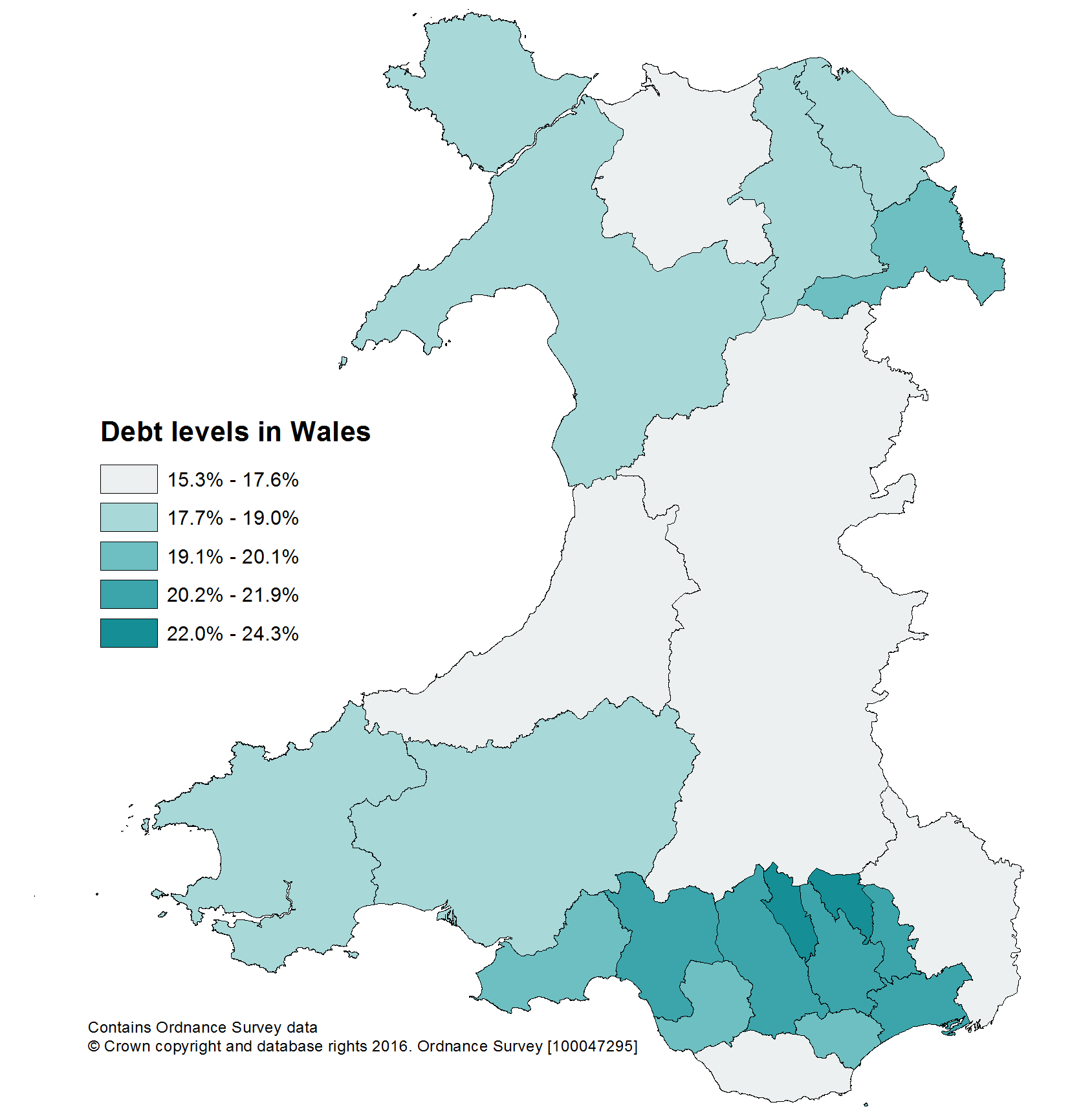

Almost one in five people in Wales is living with problem debt, compared to a UK average of one in six. Research published by the Money Advice Service shows that indebtedness has increased in Wales from 16% in 2014 to 19.6% in 2016, while the UK average has fallen from 18% to 16% over the same period. [caption id="attachment_6543" align="alignright" width="287"] Contains Ordnance Survey data. Crown copyright and database rights 2016. Ordnance Survey [100047295].[/caption]Three of the 10 UK local authorities with the highest level of over-indebted residents are in Wales:

Contains Ordnance Survey data. Crown copyright and database rights 2016. Ordnance Survey [100047295].[/caption]Three of the 10 UK local authorities with the highest level of over-indebted residents are in Wales:

- Blaenau Gwent (second at 24.3%);

- Merthyr Tydfil (third at 24.1%); and

- Rhondda Cynon Taf (tenth at 21.9%).

- Monmouthshire (15.3%) is the only local authority in Wales where the level of over-indebtedness is lower than the UK average.

Socio-economic factors

Why are there such high levels of indebtedness in some parts of the country? There is no one simple answer, but the figures above, along with analysis by the Public Policy Institute for Wales (PPIW), demonstrate the link between debt and socio-economic disadvantage. Blaenau Gwent, Merthyr Tydfil, Rhondda Cynon Taf and Caerphilly all have high levels of debt and insolvency. These are mirrored by high levels of welfare dependency, below-average incomes and high levels of multiple deprivation. While there is a clear relationship between socio-economic deprivation and over-indebtedness, others factors, including the effect of financial exclusion, should not be overlooked.

Financial exclusion

Financial exclusion is characterised by limited access to mainstream financial services, such as bank accounts and credit. As a result some individuals depend on high-cost lending, cannot benefit from direct debit discounts, and must pay to access their money as they live in areas with no free cash machines. Such factors may not be the root cause of indebtedness but they do exacerbate financial difficulties.

Improving access to financial services

The UK Government and the finance industry have taken action to improve access to financial services. Examples include:

- an agreement between the UK Government and the banking industry means that nine major banks and building societies offer basic bank accounts to people who cannot access a traditional bank account;

- in 2006, LINK identified priority areas across the UK for installing free cash machines. It has expanded this programme, and 202 of the new priority areas awaiting installation are in Wales;

- traditional sources of loans such as banks and credit unions are competing with high-cost lenders who offer fast access to short-term loans. Smart Money Cymru is among the credit unions now making decisions on loans on the same day as the application is received; and

- banks and building societies provide easy access accounts for short-term saving, while some credit unions work with local employers to provide a payroll deduction scheme for employees to pay directly from their salary into a savings account.

Credit Unions

A credit union is a non-profit making financial co-operative whose members can access credit at low interest rates. Members of a credit union save in a common fund, which can be used to offer affordable loans. The income generated through lending is used to meet the credit union’s operating expenses, build reserves and pay dividends to savers.

The previous Welsh Government’s approach

The Financial Inclusion Strategy for Wales 2016 describes the previous Welsh Government’s vision for a financially inclusive Wales. It notes that to bring about this vision people must have, among other things, access to affordable credit and financial services. The strategy makes a number of commitments to tackle financial exclusion, stating the Welsh Government will:

- work with key partners to ensure everyone has access to a basic bank account;

- work to ensure free cash machines are installed in priority areas as a matter of urgency;

- work with credit unions to improve access to affordable short-term credit; and

- work with credit unions to encourage the take-up of payroll deduction for savings.

Are such actions sufficient to tackle the problems of debt and financial exclusion in Wales? Or does Wales need to develop a more distinctive, innovative approach?

Developing a new approach

The Centre for Social Justice’s report, Future Finance: A New Approach to Financial Capability, takes a different view from that of the previous Welsh Government. It says that:

- politicians and financial companies must change the way they approach low-income households. They must see them as a different type of customer, rather than as people who must be served due to social welfare policy;

- people on low incomes require better products than those currently available, and products that are designed specifically for their needs; and

- people on low incomes have the same desire for product choice as any other group. There is demand for new affordable financial products, specifically designed to serve this market.

The importance of co-operation

Regardless of the approach the new Welsh Government takes, it will continue to face a serious constraint in tackling debt and financial exclusion. This is because matters such as financial services regulation and monetary policy are not devolved. It means that tackling debt and financial exclusion not only depends on the actions taken by the Welsh Government, but also on those taken by the UK Government and the banks. Despite this, debt and financial exclusion are issues that Assembly Members in the Fifth Assembly may be unable to ignore.

Key Sources

- The Centre for Social Justice, Future Finance: A New Approach to Financial Capability (2015)

- The Money Advice Service, A Picture of Over-Indebtedness (2016)

- Public Policy Institute for Wales, Overview of Indebtedness, Low Income and Financial Exclusion (2014)

- Welsh Government, Financial Inclusion Strategy for Wales (2016)