On 2 March, the Prime Minister provided the most detail yet on what she wants the UK’s relationship with the EU to look like after Brexit. “In certain ways”, she said, “our access to each other’s markets will be less than it is now”. This is consistent with her stated desire to leave the EU Single Market and Customs Union, which she deems incompatible with the UK Government’s negotiating “red lines”.

On 23 March the European Council agreed guidelines on the framework for the future relationship with the UK. These stated that “being outside the Customs Union and Single Market will inevitably lead to frictions in trade”, whilst affirming that it was aiming for a “wide-ranging free trade agreement” … “with the aim of covering all sectors and seeking to maintain zero tariffs”. However, the Council states that such an agreement will only be possible if it includes “robust guarantees which ensure a level playing field”: i.e. does not enable the UK to seek a competitive advantage by undercutting the EU in areas including “competition and state aid, tax, social, environment and regulatory measures and practices”.

As some clarity begins to emerge on the future nature of the EU-UK relationship, what impact is this likely to have on the Welsh economy?

Professor Perdikis of Aberystwyth University has recently completed a fellowship with the National Assembly for Wales, looking – along with co-author Professor Khorana of Bournemouth University – at the likely economic impact of Brexit on Wales. This follows the Welsh Government’s publication of its Brexit trade policy, underpinned by work it had commissioned from the Welsh Economy Research Unit at Cardiff Business School (EU Transition and Economic Prospects for Large and Medium Sized Firms in Wales). These documents give an indication of the scale of the impact Brexit may have in Wales, and which sectors would be most affected.

Market access vs obligations

Different trading agreements – from membership of the EU Single Market to a Free Trade Agreement such as the CETA between the EU and Canada – represent a sliding scale of market access and reciprocal obligations. For example, Norway is not an EU member, but its membership of the Single Market entails it accepting free movement of people and making significant contributions to the EU budget. Canada has neither of these obligations, but accordingly has less access to the Single Market: the deal does not cover services, which in 2016 accounted for 35% of Welsh exports to the EU.

Different attempts to model the economic impacts of Brexit have therefore picked different points on this sliding scale, and estimated the impact of each on the UK economy. Perdikis and Khorana chose three scenarios which they viewed as being compatible with the UK Government’s stated “red lines” (Control of immigration; ability of the UK to make its own free trade agreements; independence from the European Court of Justice; and an end to substantial contributions to the EU budget) and looked at their likely impact on the Welsh economy:

- No deal with the EU. In the absence of a deal, the EU and UK would trade together on World Trade Organisation terms from March 2019;

- An agreed “status quo” transition period of varying lengths, whereby the EU and UK agree to continue trading under current terms;

- A comprehensive EU-Canada style (“CETA-style”) free trade agreement between the EU and UK.

Although the UK-EU relationship will probably look different to any existing relationship between a third-party country and the EU, these points can be used to indicate the likely impact of this new relationship on the Welsh economy, based on its degree of resemblance to these existing or theoretical relationships. Their report goes through in detail the estimated outcomes of these scenarios on the Welsh economy using indicators such as GDP, trade volumes and employment.

A deal is better than no deal

Perdikis and Khorana conclude:

The scenario simulations reveal that Brexit will lead to the imposition of costs, either through the imposition of tariffs or the loss of preferential access to the single market. The impact on the Welsh economy will be felt via reductions in GDP, GDP per capita, trade, investment and employment. The least costly outcome for Wales is if the status quo can be held to for as long as possible. The next best or next least worst is the conclusion of a CETA type agreement by the EU. The most costly is a Brexit based on WTO rules.

These results, they state “chime with both economic theory and empirical work carried out by the majority of other researchers”. Moving from a state of relatively free trade – as the UK currently has with the EU - to one involving more barriers will “inevitably lead to losses in economic welfare”. This view is consistent with the EU Exit Analysis Cross Whitehall Briefing, which sees a range of GDP losses resulting from Brexit the further the UK moves from its current level of Single Market access. Perdikis and Khorana note that the order of magnitude of the GDP losses they predict are significantly smaller than those predicted in other mainstream forecasts as their methodology focused on a limited set of Brexit impacts. “Had our study included these aspects”, they state “it is likely that the losses we identify would have been larger and more in line with their results”.

The widespread view is that the forms of Brexit above amount to forms of damage limitation. This has led to some calls – notably from Economists for Free Trade and Policy Exchange – for the UK to unilaterally remove its tariffs to reduce the costs of imports and boost UK competitiveness. Perdikis and Khorana suggest a number of problems with this proposal, including a misunderstanding of the relationship between EU regulations and prices. Furthermore, such an approach would most likely lead to a decline in manufacturing and agriculture in the UK, which the report authors state would have an “adverse impact on the distribution of income” with “economic and social impacts on Wales” which “could be very severe in the short to medium term”.

Welsh Government’s trade policy: full and unfettered access to the Single Market

The Welsh Government’s Trade Policy paper reiterates its call for “continued full and unfettered access to Europe’s Single Market” and remaining in the EU Customs Union “at least for the foreseeable future”. Perdikis and Khorana note that this aim is consistent with their research suggesting economic losses arising from losing access to the Single Market.

The Welsh Government’s preferred model would prevent the UK from having an independent trade policy. As a member of the EU Customs Union it would need to maintain the same set of tariffs as the EU, and could not independently conclude trade deals. In this manner it cuts across one of the UK Government’s red lines, and as such is not directly analysed in Perdikis and Khorana’s report. Any suggestion, the Welsh Government states, that free trade deals with third party countries could compensate for loss of access to the Single Market “would need to be supported by evidence, and to date no evidence has been published by the UK Government to support this view”.

Sectors at risk in Wales

The Welsh Government’s policy paper is supported by a report from Cardiff University Business School focussing on the Economic Prospects for Large and Medium Sized Firms in Wales of Brexit. The research was conducted largely through the lens of the Welsh Anchor and Regionally Important Companies (“Anchor Companies” are international companies with a significant presence in Wales), and addressed questions including:

- How post-Brexit options would affect large and medium sized firms in Wales, and which sectors could be most vulnerable to the EU transition process?

- What might EU transition processes mean for inward investment and trade in sectors?

- What would a change in investment levels or output mean for other parts of the regional economy (i.e. supply chain and household effects)?

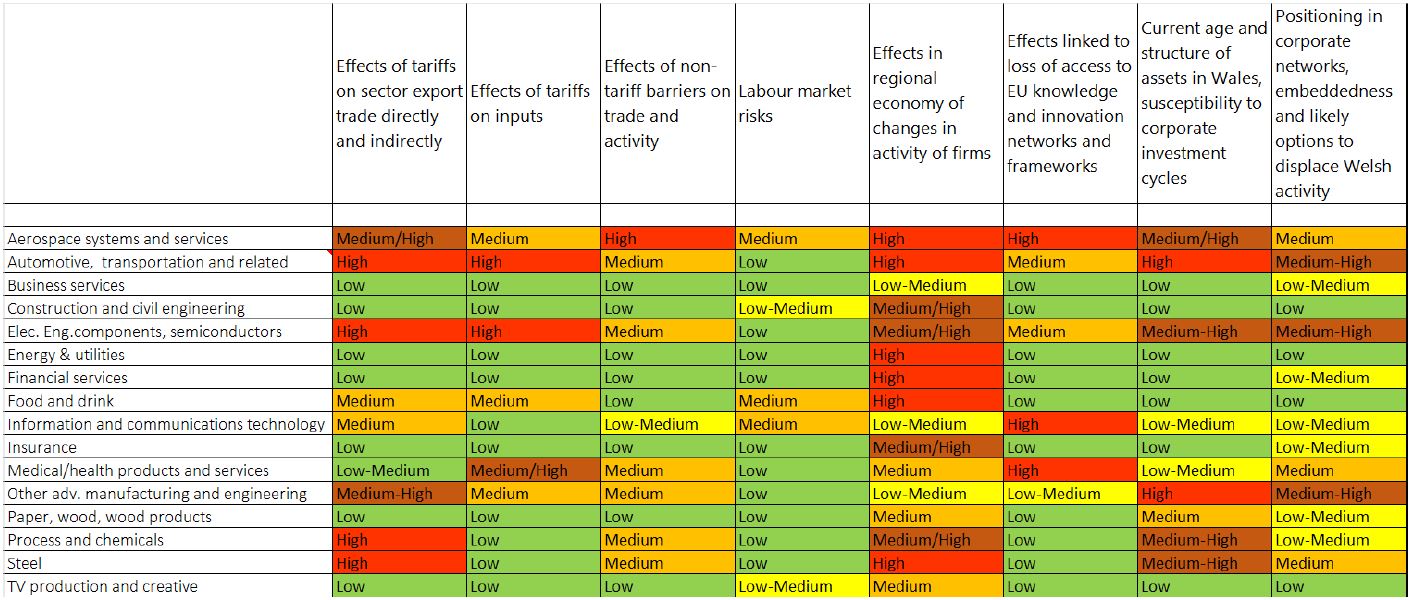

The Cardiff University report included the following table, summarising the risks associated with Brexit for different sectors in the Welsh economy: Summary of how different sectors were rated on different aspects of risk  The report states that “few respondents were able to comment on any new opportunities presenting themselves as result … of a hard Brexit and trading on WTO rules”.

The report states that “few respondents were able to comment on any new opportunities presenting themselves as result … of a hard Brexit and trading on WTO rules”.

On 27 March the National Assembly for Wales’s External Affairs and Additional Legislation Committee (the committee monitoring the Brexit process) published its report into Wales’s future relationship with the EU. This stated that “The future relationship with the European Union must prioritise frictionless trade, free from tariff and non-tariff barriers after Brexit”. The UK is set to exit the EU in under a year. As more clarity emerges on what Brexit may look like and what impact it may have, politicians in the Assembly will continue to press the Welsh Government to do what it can to secure a Brexit that works for Wales.

Article by Robin Wilkinson, National Assembly for Wales Research Service

Source: Cardiff University Business School, EU Transition and Economic Prospects for Large and Medium Sized Firms in Wales