The annual accounts for 2016-17 of National Health Service (NHS) bodies in Wales are the first to report performance against the first statutory financial duty introduced by the National Health Service Finance (Wales) Act 2014.

The annual accounts for 2016-17 for the seven Local Health Boards (LHBs) and three NHS Trusts in Wales were laid by the Auditor General for Wales at the National Assembly for Wales on 9 June 2017.

What are the statutory financial duties?

Under the National Health Service (Wales) Act 2006, each LHB in Wales was required to ensure that the use of its resources in a financial year did not exceed the spending limits set for it in relation to that year by Welsh Ministers.

On 1 April 2014, the National Health Service Finance (Wales) Act 2014 amended the National Health Service (Wales) Act 2006, replacing the duty to balance the books each and every year with a requirement on LHBs to manage their resources within approved limits over a three-year rolling period. This is known as the first statutory financial duty. It was envisaged that this change in requirement would give LHBs in Wales the flexibility needed to enable more long-term service, financial and workforce planning, as well as helping to ensure the sustainable transformation of healthcare services.

Financial planning in response to the 2014 Act is underpinned by the second statutory duty, which requires that each LHB prepares and has approved by Welsh Ministers a rolling three-year Integrated Medium Term Plan (IMTP).

Welsh Health Circular WHC/2016/054 clarified the statutory financial duties of NHS bodies in Wales and confirmed that, while the change of legislation introduced by the National Health Service Finance (Wales) Act 2014 related to LHBs, the two financial duties also applied to Welsh NHS Trusts.

How will performance against the first financial duty be measured?

Schedule 9 of the National Health Service (Wales) Act 2006 requires LHBs and NHS Trusts to prepare annual accounts. Section 61 of the Public Audit (Wales) Act 2004 requires that these annual accounts are examined and certified by the Auditor General for Wales, who is also responsible for laying a copy of the certified accounts before the National Assembly for Wales. The annual accounts of LHBs and NHS Trusts report their performance against the two financial duties.

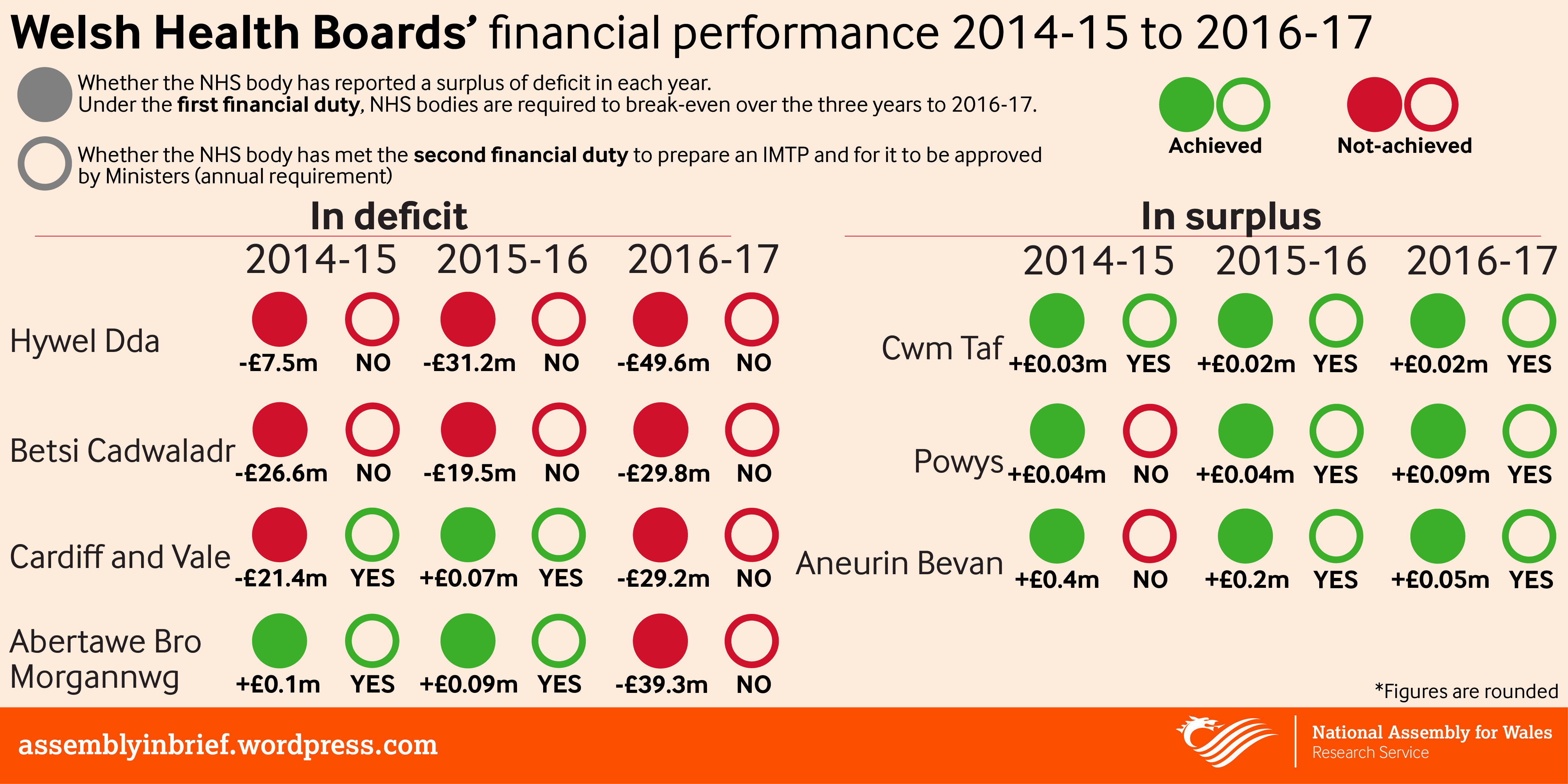

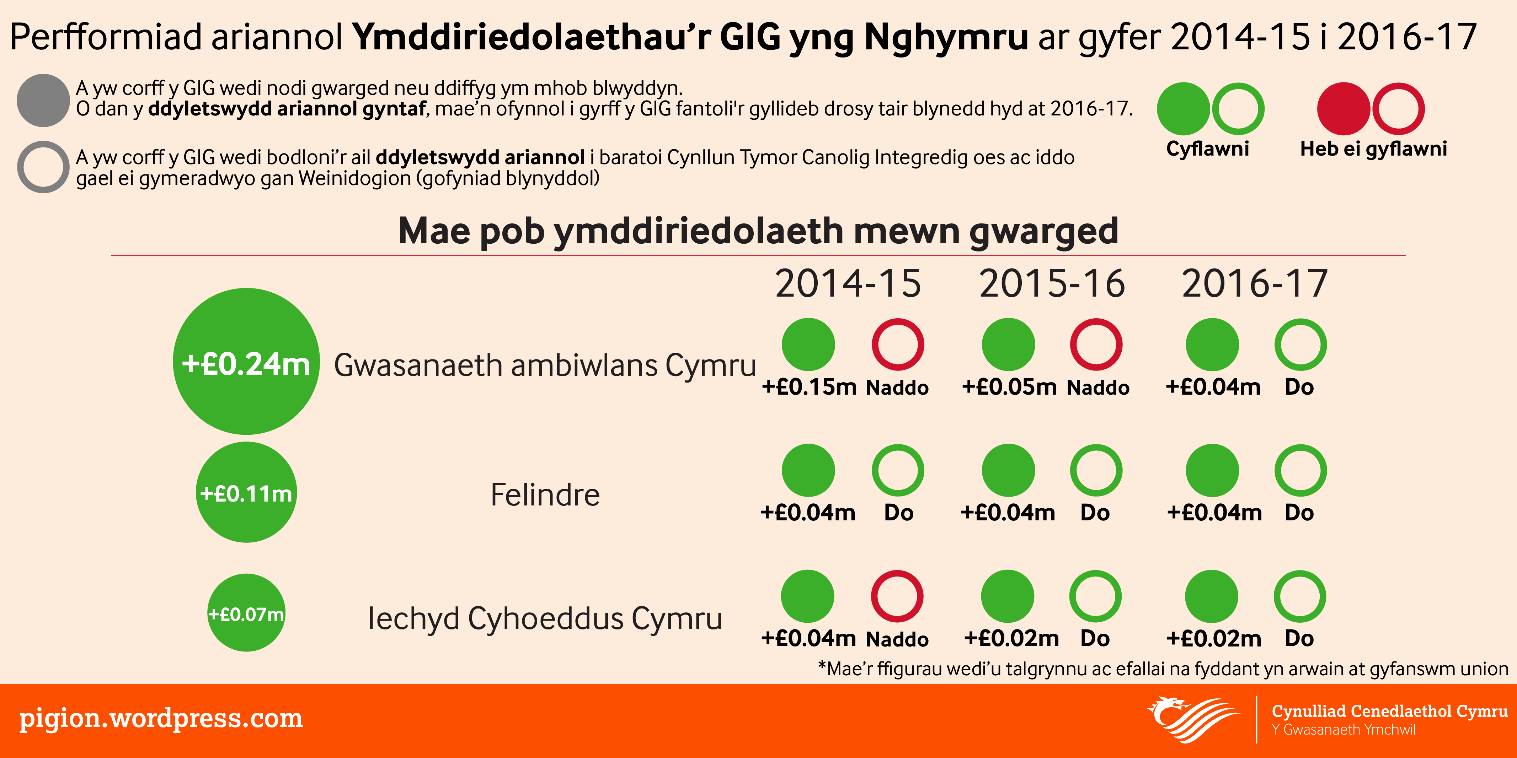

Have LHBs and NHS Trusts met the first financial duty?

The first three-year period under the first financial duty ran from 2014-15 to 2016-17. Performance against this duty is assessed for the first time in 2016-17 and reported in the annual accounts for 2016-17.

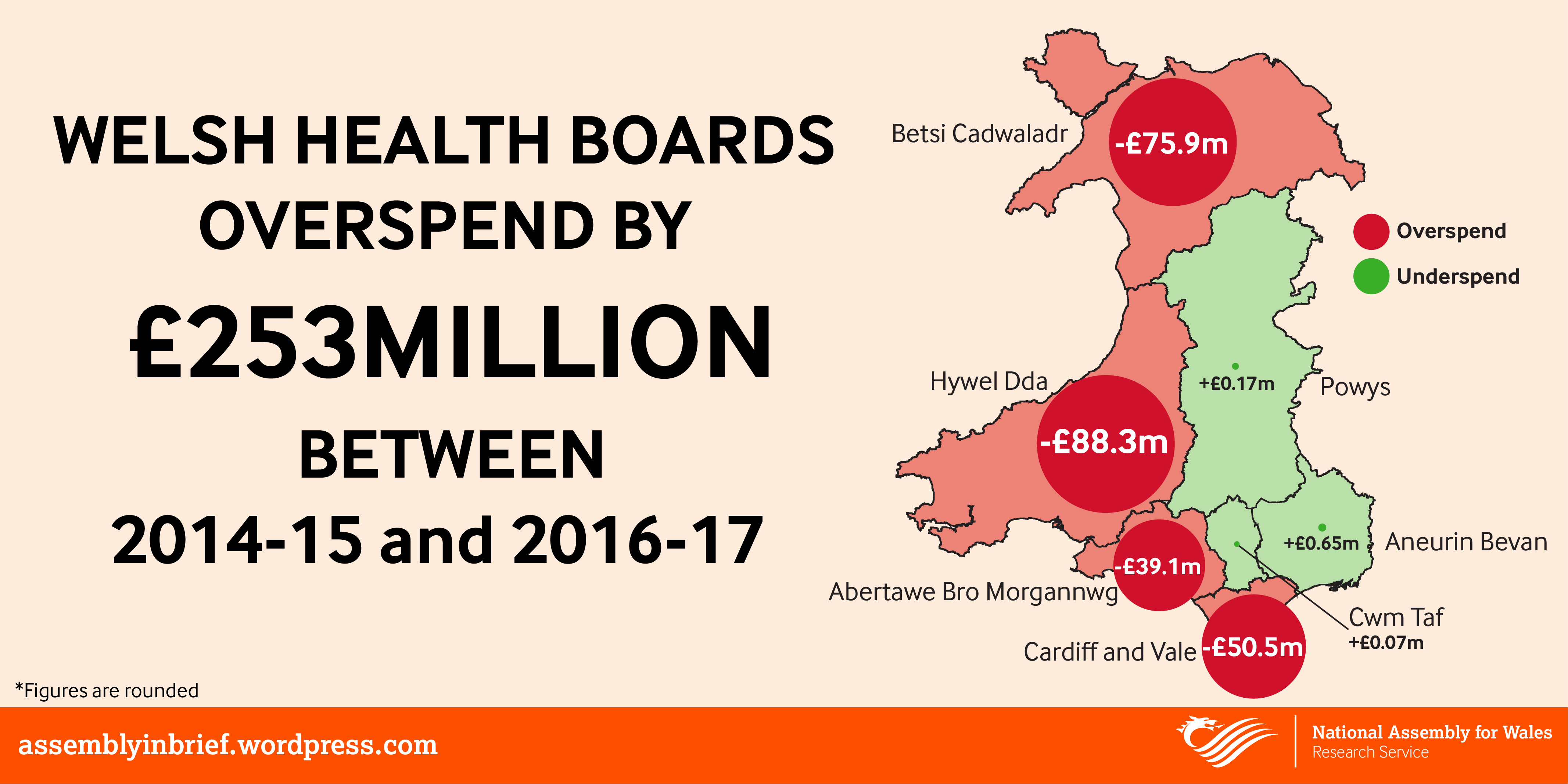

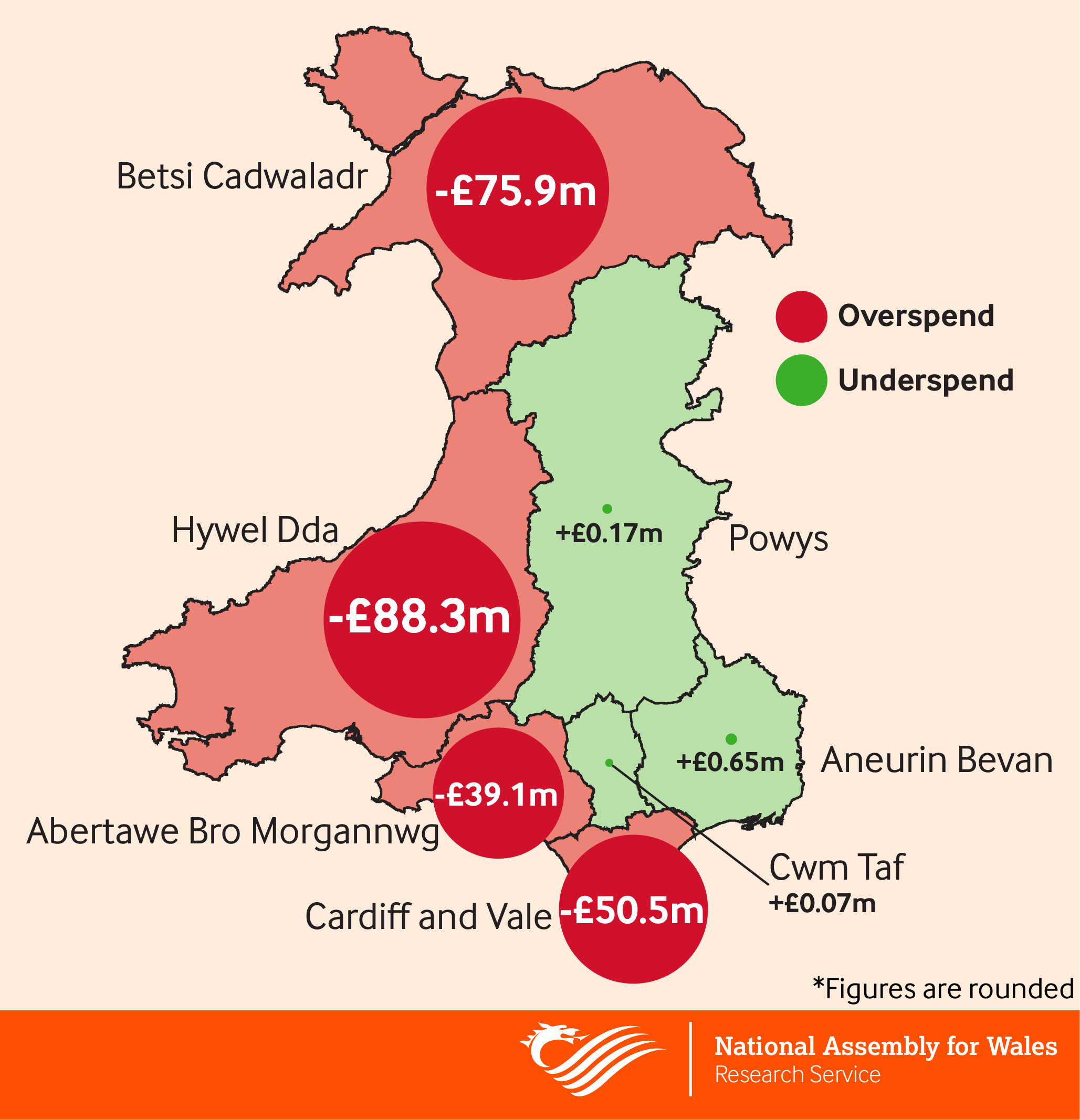

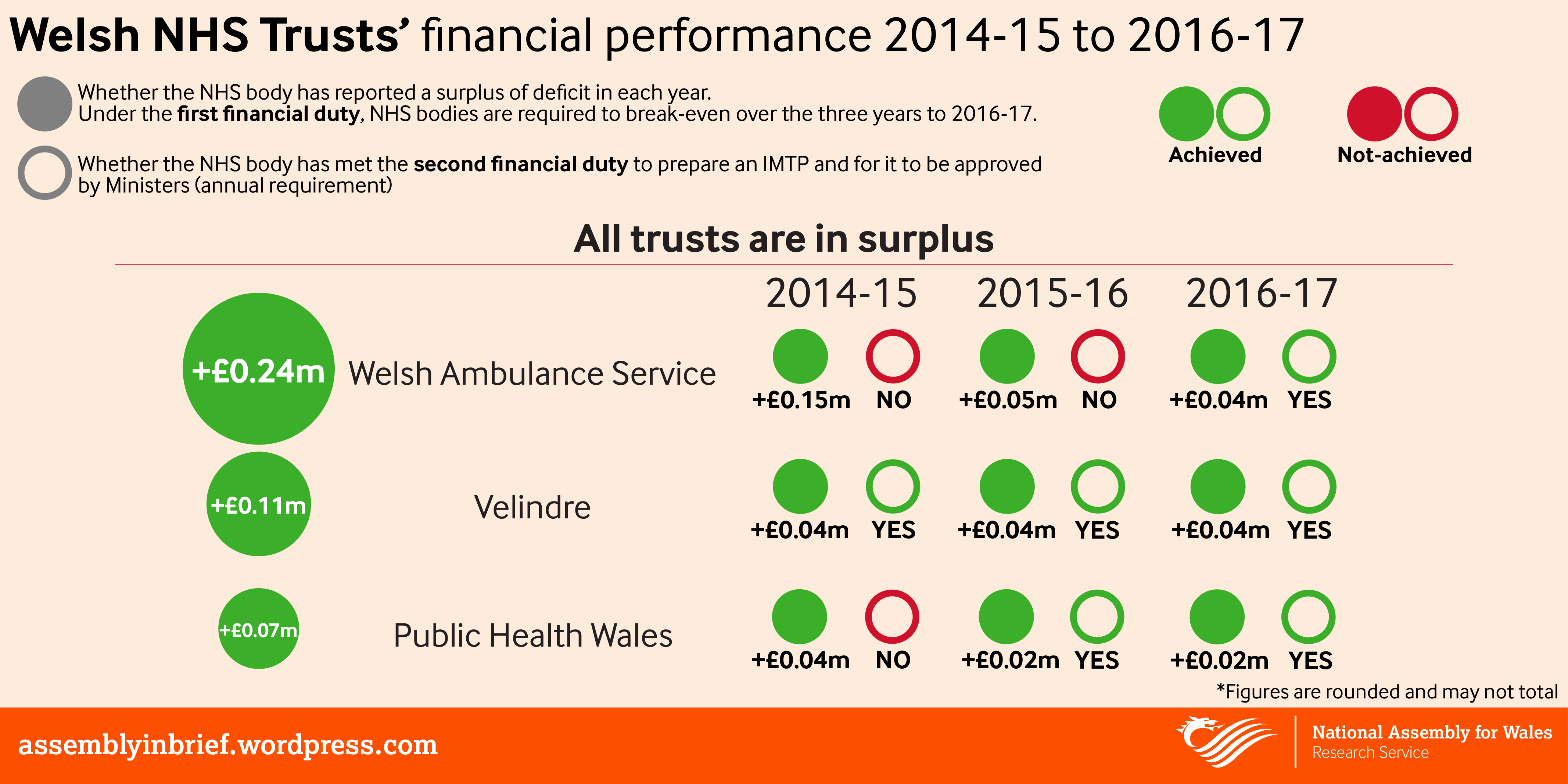

All NHS trusts in Wales met the first statutory duty by balancing their books. However, this was not the case for all LHBs. Only three LHBs reported that they had met the first statutory financial duty by operating within their revenue spending limit over the three-year period 2014-15 to 2016-17. The remaining four LHBs did not meet the first duty, reporting an overspend over the three years 2014-15 to 2016-17. The aggregate position for all LHBs for the three-year period to 2016-17 was a net overspend of £253 million. The reported position against the revenue spending limit for each LHB is shown below:

All seven LHBs stayed within their limits for capital spending over the three-year period 2014-15 to 2016-17.

Have LHBs met the second financial duty?

The annual accounts for NHS bodies in Wales from 2014-15 onwards report whether LHBs and NHS Trusts have met the second financial duty. The performance is summarised below:

A number of these NHS bodies, whilst not having had a three year IMTP approved, have submitted a one-year plan.

What is the impact of the reported deficits?

Paragraph 22, Enclosure 1 of Welsh Health Circular WHC/2016/054 notes that:

Failure to achieve the first financial duty is viewed as a serious matter by the Welsh Government and will be considered in accordance with the NHS Wales Delivery Framework included annually in the IMTP guidance and the escalation and intervention arrangements in the NHS in Wales.

In a written statement on 9 June 2017, the Cabinet Secretary for Health, Wellbeing and Sport, Vaughan Gething AM, set out how the Welsh Government had responded to the financial performance concerns in the four LHBs that reported an overspend in the three-year period 2014-15 to 2016-17. This included monitoring of their financial performance and undertaking financial governance reviews. The Cabinet Secretary noted that “these reviews have recently concluded, and we will be considering the lessons to be learned and follow-up action required early in this financial year”.

The Cabinet Secretary also reported that:

Additional cash support has continued to be provided when required to all Boards in deficit to enable them to meet their normal cash commitments including payroll expenditure. This cash assistance is repayable in future financial years when appropriate and improved plans are developed and approved under the Act to enable the repayment of deficits.

The requirement to repay the cash assistance and overspends will add to existing financial pressures on LHBs in the short and long term. The first financial duty is to be assessed on a rolling three-year period. Therefore, any overspends reported for 2015-16 and 2016-17 will be assessed next year with LHB’s financial performance in 2017-18. The value of the total overspend reported by four LHBs for 2015-16 and 2016-17 is £198 million.

NHS Wales is facing long term funding and sustainability pressures including an increasingly ageing population with increased morbidity, a growing rate of obesity and related conditions and developments in technology leading to more complex treatments coming on line.

A number of recent reports have highlighted the pressures facing healthcare in Wales. The Health Foundation report The path to sustainability: Funding projections for the NHS in Wales to 2019/20 and 2030/31 (October 2016) stated that the NHS in Wales is “facing the most financially challenging period in its history” and the savings needed are “extremely challenging”. The report set out that NHS Wales needed additional funding, but also improved efficiency and services adapted to meet changing patient needs.

Similarly, the Public Policy Institute for Wales report Efficiency and the NHS Wales Funding Gap (October 2016) identified the need for improved efficiency and service change, but also for a more strategic and sustained national approach to improving efficiency and supporting change. The Welsh NHS Confederation have also highlighted the financial pressures facing NHS Wales and argued that there will need to be some difficult choices made on future services and priorities in an environment where finances will continue to be extremely tight.

The Cabinet Secretary’s written statement of 9 June 2017 reports that he is confident that the health and social services budget has broken even overall in 2016-17. At the same time, the evidence suggests that ongoing and future financial challenges remain.

Article by Dr Paul Worthington and Joanne McCarthy, National Assembly for Wales Research Service.

This post is also available as a print-friendly PDF: A financial health check – have local health boards and NHS Trusts in Wales met their financial duties? (PDF, 407KB)

{kind=link}